Strong income alone doesn’t create wealth. Money management does. In 2026, rising living costs, subscription-based spending, and digital payment convenience make it easier than ever to lose track of where money goes.

Effective money management isn’t about restriction. It’s about control, clarity, and consistency. When your financial decisions are intentional, stress decreases — and long-term progress becomes measurable.

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.

What Money Management Really Means

Money management is the system you use to:

- Track income

- Control expenses

- Build savings

- Reduce debt

- Invest strategically

For example, someone earning $6,000 per month may feel financially strained — until they realize $900 disappears into unused subscriptions, dining, and impulse purchases. Clarity changes behavior.

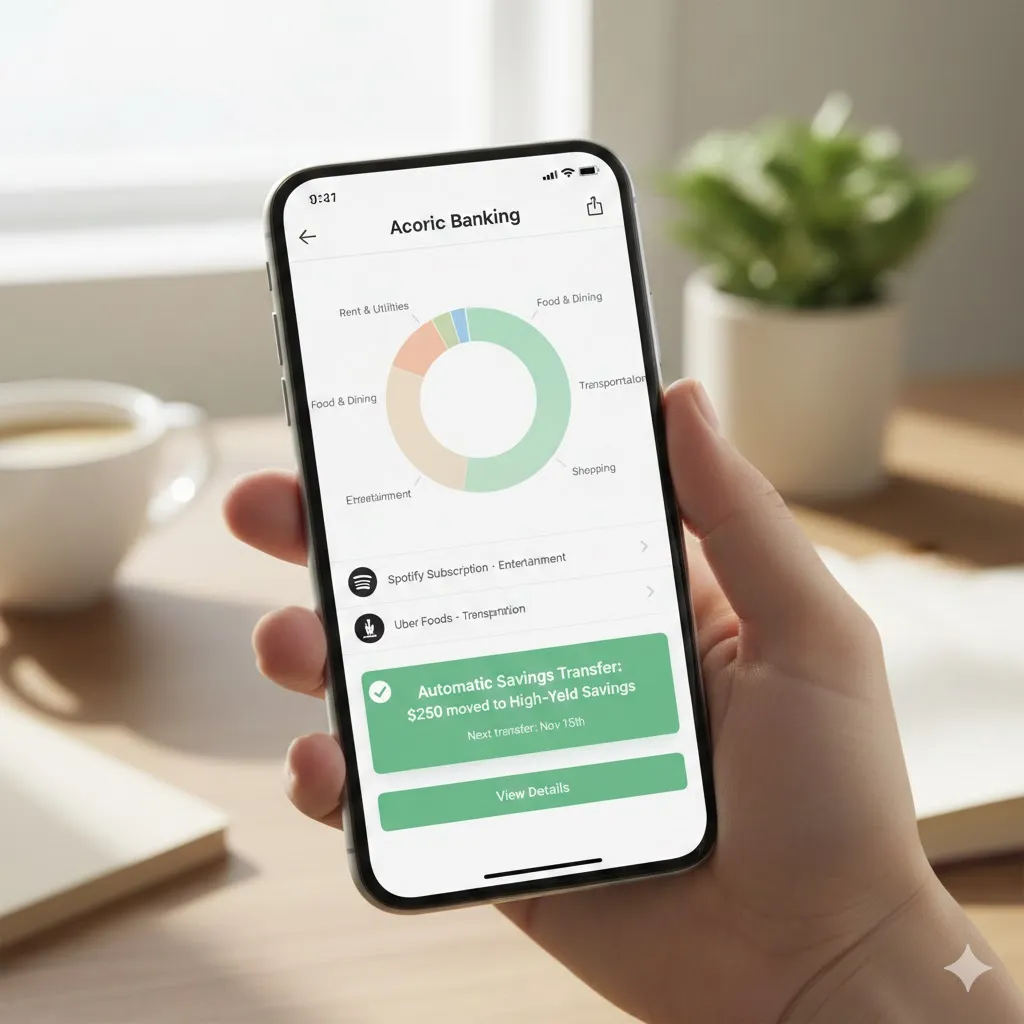

Step 1: Build a Clear Spending Framework

A simple structure makes money decisions easier.

Fixed Expenses

These include rent, mortgage, insurance, and loan payments.

Variable Expenses

Groceries, transportation, and utilities fluctuate monthly.

Discretionary Spending

Dining out, entertainment, travel, and shopping.

| Category | Purpose | Financial Impact |

|---|---|---|

| Essentials | Maintain daily living | Stability |

| Savings | Emergency & long-term goals | Security |

| Investments | Wealth growth | Future income |

| Debt Payments | Reduce interest burden | Financial freedom |

Organizing spending into categories reveals patterns quickly.

Step 2: Automate Financial Discipline

Automation reduces decision fatigue.

Pay Yourself First

Schedule automatic transfers to savings or investment accounts on payday.

Automate Bill Payments

Avoid late fees and protect credit scores by setting up autopay.

Increase Savings Gradually

When income rises, raise your savings rate before increasing lifestyle expenses.

Small automated improvements compound over time.

Pro Insight

Consistency beats intensity. Saving 15% steadily for 10 years often outperforms short bursts of aggressive saving followed by inconsistency.

Step 3: Manage Debt Strategically

High-interest debt slows progress dramatically.

Focus on:

- Paying off high-APR credit cards

- Avoiding unnecessary financing

- Refinancing when interest rates improve

For example, reducing a 20% APR credit card balance frees up future cash flow for savings and investing.

Step 4: Invest With Purpose

Once savings and debt are under control, investing supports long-term growth.

Diversify Assets

Spread investments across asset classes to reduce concentration risk.

Reinvest Returns

Compounding strengthens long-term outcomes.

Stay Disciplined

Market volatility is normal. Emotional reactions often harm returns more than market movements themselves.

Long-term investing requires patience.

Step 5: Review Regularly

Money management is not a one-time setup.

Review monthly:

- Spending trends

- Savings progress

- Investment allocation

- Debt balances

Quarterly reviews help adjust goals and prevent financial drift.

Quick Tip

Track every expense for one full month without judgment. Awareness alone often reduces unnecessary spending.

Frequently Asked Questions

How much should I save each month?

Many experts suggest 15–20% of income when possible, though personal circumstances vary.

Should I focus on saving or investing first?

Build an emergency fund first, then shift toward long-term investing.

Is budgeting necessary for high earners?

Yes. Higher income often increases spending unless controlled intentionally.

How often should I review finances?

Monthly reviews are effective, with deeper quarterly evaluations.

What’s the biggest money management mistake?

Lack of consistency. Sporadic effort rarely produces strong long-term results.

Conclusion

Money management in 2026 is about structure, automation, and steady discipline. By organizing expenses, reducing high-interest debt, building savings, and investing consistently, you create financial stability that grows over time.

Control your money — or it will quietly control you.

Trusted U.S. Resources

Consumer Financial Protection Bureau (CFPB) – Budgeting Tools

https://www.consumerfinance.gov/

U.S. Securities and Exchange Commission (SEC) – Saving and Investing

https://www.sec.gov/

Federal Trade Commission (FTC) – Credit and Debt Resources

https://consumer.ftc.gov/

USA.gov – Financial Services and Benefits

https://www.usa.gov/