Building long-term wealth isn’t about chasing trends or quick wins. It’s about creating a system that grows steadily, withstands downturns, and supports your goals for decades.

In 2026, rising living costs, evolving tax rules, and volatile markets make disciplined financial planning more important than ever. Long-term wealth is not built overnight — it’s constructed intentionally through smart habits and consistent decisions.

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.

What Long-Term Wealth Really Means

Long-term wealth goes beyond income. It includes:

- Appreciating investments

- Income-generating assets

- Retirement accounts

- Real estate holdings

- Business ownership

- Diversified financial reserves

For example, someone earning a high salary but spending most of it may not build wealth. Meanwhile, a disciplined saver investing consistently over 20 years often achieves financial independence.

Wealth is built on assets — not just earnings.

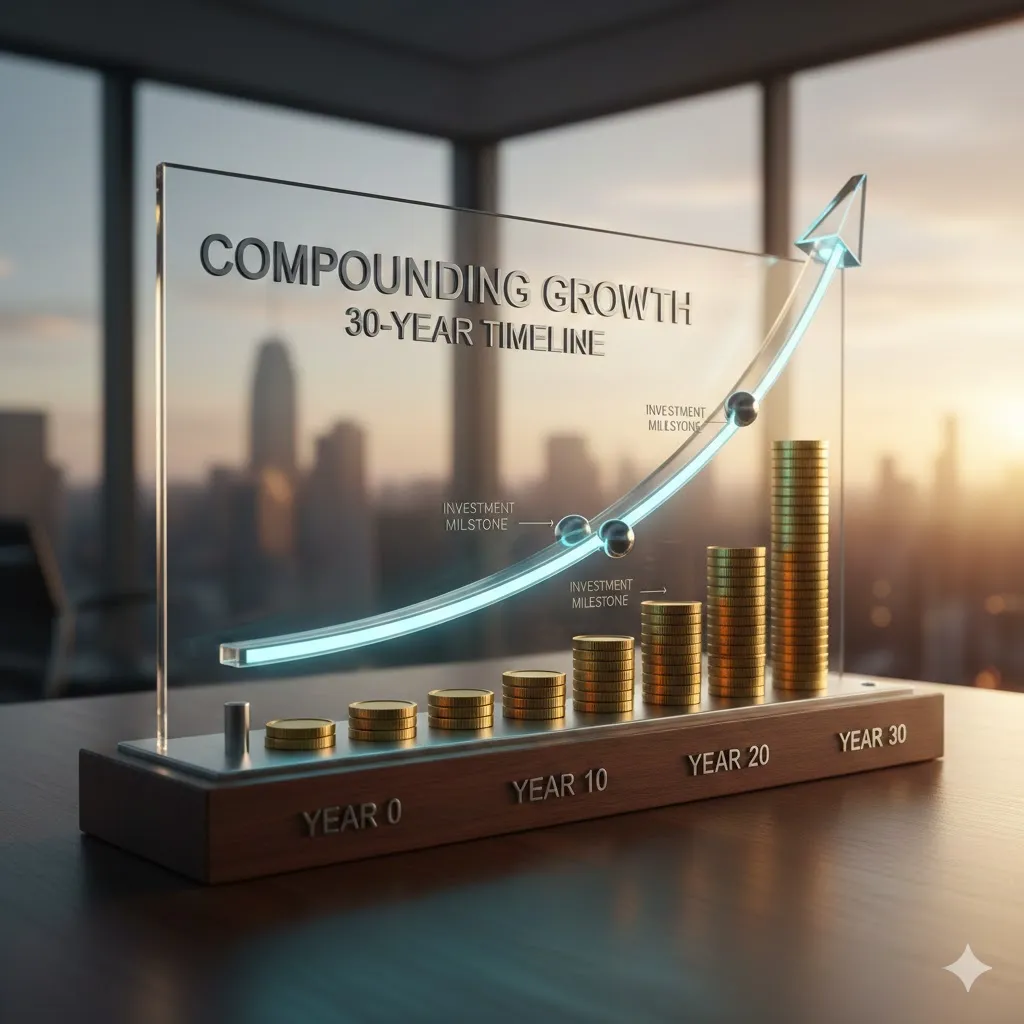

The Power of Compounding

Compounding allows investments to generate returns on both the original amount and previous gains.

Consider this simplified example:

- Invest $10,000

- Earn 7% annually

- Leave it untouched for 20 years

Growth accelerates because returns build upon prior returns.

| Investment Period | Initial Investment | Estimated Growth at 7% |

|---|---|---|

| 5 Years | $10,000 | ~$14,000 |

| 10 Years | $10,000 | ~$19,700 |

| 20 Years | $10,000 | ~$38,700 |

| 30 Years | $10,000 | ~$76,100 |

Time is often more powerful than timing.

Core Pillars of Long-Term Wealth

Consistent Investing

Regular contributions to diversified portfolios support steady growth.

Asset Diversification

Spreading investments across stocks, bonds, and real assets reduces concentration risk.

Debt Management

High-interest debt slows wealth accumulation. Eliminating it accelerates progress.

Tax Efficiency

Using tax-advantaged accounts — such as retirement plans — may improve long-term outcomes.

Each pillar reinforces the others.

Pro Insight

Increasing your savings rate by just 5% — and investing the difference consistently — often impacts long-term wealth more than attempting to outperform the market.

Protecting Wealth Over Time

Building wealth is only half the equation. Protecting it matters just as much.

Emergency Fund

Maintaining liquidity prevents forced liquidation of investments during downturns.

Insurance Planning

Health, disability, and property insurance protect against financial setbacks.

Estate Planning

Wills and trusts help transfer assets efficiently and according to your wishes.

Long-term wealth requires both growth and defense.

Avoiding Common Wealth-Building Mistakes

Emotional Investing

Reacting to short-term market swings often disrupts long-term strategies.

Lifestyle Inflation

Increasing spending every time income rises slows asset accumulation.

Overconcentration

Relying heavily on a single asset class increases vulnerability.

Sustainable growth requires discipline.

Quick Tip

Automate investment contributions so wealth-building happens consistently — regardless of market headlines.

Frequently Asked Questions

How long does it take to build long-term wealth?

It varies by income, savings rate, and investment performance, but most wealth-building plans span decades.

Is real estate necessary for long-term wealth?

Not mandatory, but real estate can diversify income sources and assets.

Should I invest aggressively when young?

Asset allocation should reflect time horizon and risk tolerance.

Can average earners build wealth?

Yes. Consistency and savings rate often matter more than income level.

What’s the biggest factor in long-term wealth?

Time in the market and disciplined contributions.

Conclusion

Long-term wealth in 2026 is built through consistent investing, diversified assets, disciplined saving, and strategic protection. It’s not about chasing fast gains — it’s about compounding steady progress over time.

Build gradually. Protect wisely. Let time work in your favor.

Trusted U.S. Resources

U.S. Securities and Exchange Commission (SEC) – Investor Education

https://www.sec.gov/

Consumer Financial Protection Bureau (CFPB) – Financial Planning Tools

https://www.consumerfinance.gov/

Internal Revenue Service (IRS) – Retirement Plans Information

https://www.irs.gov/

USA.gov – Financial Services and Benefits

https://www.usa.gov/